December 2024

Plan Sponsor News

Welcome to the December 2024 issue of Plan Sponsor News! In this quarterly issue, prepare for the new year by reading about SECURE 2.0 Act key provisions, common plan administration mistakes to avoid and tips to guide your employees to make the most of their retirement plans.

SECURE 2.0 Act: What’s Coming in 2025

On December 10, Mutual of America Financial Group held a webinar covering SECURE 2.0 Act key provisions and insights that plan sponsors need to know about for 2025, including:

- An update on IRS guidance for provisions in effect, including student loan payments and inherited IRAs, plus changes to RMD rules

- Automatic enrollment in new plans and expanded LTPT worker coverage

- Enhanced catch-up contributions and exceptions to early distribution penalty rules

- Regulatory guidance, plan administration and amendments

Watch a replay of “SECURE 2.0 Act: What’s Coming in 2025,” with speakers Nick Curabba, Senior Vice President and Associate General Counsel, Earl Jones, Vice President, National Accounts, and moderator Kieran O’Dwyer, Vice President, Corporate Communications, each from Mutual of America.

Contact your local Mutual of America Financial Group representative with any questions you may have about how this information may affect you and your employees.

Better your tomorrow.

Contact your Mutual of America representative today.

Plan Sponsors: How to Set Yourself Up for Success in the New Year

As a plan sponsor, you have multiple responsibilities, and making sure your retirement plan stays in compliance throughout the year is critical. Establishing a schedule throughout the year to review basic operations can help identify any issues with your 401(k) or 403(b) plan, as can being familiar with what to watch out for in the first place. Here are some common mistakes and how to avoid them.

Mistake: Late deposits of employee elective deferrals

U.S. Department of Labor (DOL) rules require plan sponsors to remit 401(k) and 403(b) plan participants’ salary reduction contributions to the plan “as soon as reasonably possible,” meaning as soon as these amounts can reasonably be segregated from their general assets.

Although there is no specific date tied to “as soon as reasonably possible,” there have been cases in which DOL audits have found remittances more than three business days after the employer would have paid the employee funds to be late. In some cases, given the availability of electronic funds transfer capabilities, one business day was considered late.

For a small plan, defined as a plan with fewer than 100 participants (including all plan participants, not just actively employed participants) as of the first day of a plan year, the DOL has created a safe harbor. For such a plan, if participant contributions and loan repayments are remitted by the seventh business day following the date the amount is deducted from the participant’s pay, the remittance will be deemed to have been segregated from the employer’s general assets as soon as could reasonably be expected.

If deposits are not made in a timely manner, it could be deemed a prohibited transaction and could lead to plan disqualification.1 Mutual of America can help with avoiding late remittances by setting up payroll integration to streamline data transfer and remittance processing. If a remittance delay has occurred, your local Client Relationship Manager (CRM) can help with the correction through the IRS’s Employee Plans Compliance Resolution System or DOL’s Voluntary Fiduciary Correction Program.

Mistake: Failure to file a Form 5500

Most plan sponsors are required to file a Form 5500 annually. Not doing so can trigger a letter from the IRS or DOL, as well as significant late-filing penalties from both regulators. The IRS penalty is $250/day up to $150,000; the DOL penalty can be as much as $2,529/day with no maximum.2

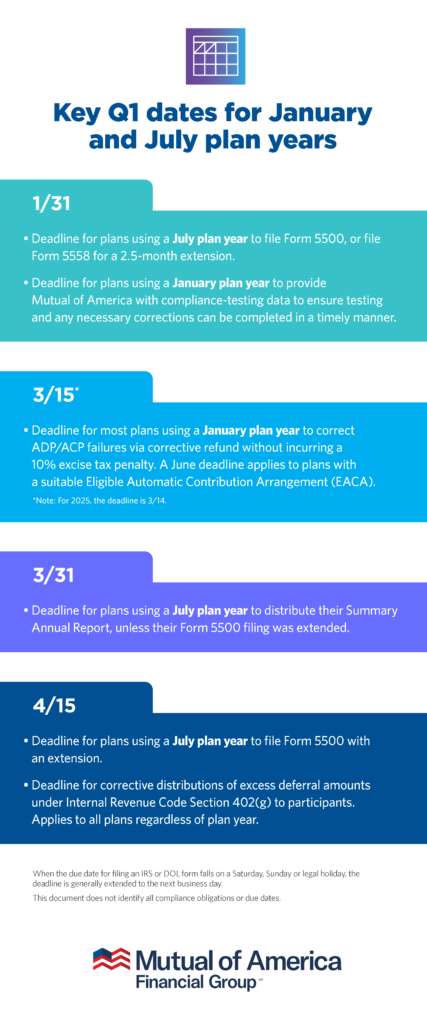

Due dates are dependent on your plan year. Know your filing deadline, and consider setting up a calendar alert for timely filing. Note: Dates apply to both 401(k) and 403(b) plans (you should adjust the date as appropriate for plan years other than January and July).

- 1/31: Deadline for plans using a July plan year to file Form 5500, or file Form 5558 for an extension

- 4/15: Deadline for plans using a July plan year to file Form 5500 with an extension

- 7/31: Deadline for plans using a January plan year to file Form 5500, or file Form 5558 for an extension

- 10/15: Deadline for plans using a January plan year to file Form 5500 with an extension2

For exclusive and coordinated services clients, Mutual of America prepares a draft Form 5500, provides a platform to electronically file it and reminds those clients of upcoming deadlines. If there is a late or missed filing, your local CRM can help bring you back into compliance by going through the DOL’s Delinquent Filer Voluntary Compliance Program (DFVCP), which may significantly reduce penalties.

Mistake: Not correcting a failed ADP and/or ACP nondiscrimination test

401(k) plan sponsors must ensure their plans don’t favor highly compensated employees over non-highly compensated employees through annual actual deferral percentage (ADP) and actual contribution percentage (ACP) tests if the plan includes an employer matching contribution. While 403(b) plans are not subject to the ADP test (they must instead comply with the “universal availability” rule), they are subject to the ACP test if they provide for an employer matching contribution. A plan failing the test has 2.5 months (six months for plans with an eligible automatic contribution arrangement) after the plan year being tested to make corrections or risk a 10% excise tax on the correction amount.3 Plan sponsors making corrections after that deadline face additional potential fines, reviews and fees.

For exclusive and coordinated services plans, Mutual of America provides a suite of compliance testing. If the plan fails an ADP or ACP test, we can provide correction methods and help you through them. Your CRM can also discuss ways to improve ADP and/or ACP test results or avoid this compliance testing altogether through plan design.

Mistake: Required minimum contributions not made to a top-heavy 401(k) plan

A 401(k) is considered top-heavy if the total value of key employees’ plan accounts is more than 60% of the total value of the plan assets as of the last day of the prior plan year. If that’s the case, an employer must contribute up to 3% of compensation for all non-key employees employed on the last day of the plan year, subject to vesting rules and adjusted for plan earnings. Corrective contributions may be able to be handled under the IRS’s Self-Correction Program.4

To determine if your plan is top-heavy, start by identifying key employees. That’s any employee (including former or deceased employees) who at any time during the plan year was:

- An officer making over $220,000 for 2024;

- A 5% owner of the business (a 5% owner is someone who owns more than 5% of the business); or

- An employee owning more than 1% of the business and making more than $150,000 for the plan year.4

Note that certain relatives of owners—spouses, parents, grandparents and children—may also be treated as owners.5

For exclusive and coordinated services plans, Mutual of America provides a suite of compliance testing. If the plan fails a top-heavy test, we can provide correction methods and help you through them. Your CRM can also discuss ways to improve top-heavy testing or avoid top-heavy testing altogether through plan design.

If you have questions or need assistance, please contact your local representative.

1https://www.irs.gov/retirement-plans/401k-plan-fix-it-guide-you-havent-timely-deposited-employee-elective-deferrals

2https://www.irs.gov/retirement-plans/401k-plan-fix-it-guide-you-havent-filed-a-form-5500-this-year

3https://www.irs.gov/retirement-plans/401k-plan-fix-it-guide-the-plan-failed-the-401k-adp-and-acp-nondiscrimination-tests

4https://www.irs.gov/retirement-plans/401k-plan-fix-it-guide-the-plan-was-top-heavy-and-required-minimum-contributions-were-not-made-to-the-plan

5https://www.irs.gov/retirement-plans/is-my-401k-top-heavy

Better your tomorrow.

Contact your Mutual of America representative today.

Help Employees Set the Stage for Financial Confidence

According to a recent survey, six in 10 workers say having an employer-sponsored retirement plan contributes a lot to their feeling of financial security.1 With that in mind, here are tips to share with your employees to help them make the most of their plan in the year ahead:

Confirm enrollment

If your plan is not set up with automatic enrollment, employees may not be aware they have to take action to be part of the plan. Review with them the steps on how to sign up—and make sure they understand how to adjust their contributions.

Take advantage of any employer match

Not all employer-sponsored retirement plans offer a match. If yours does, encourage employees to contribute as much as possible to take advantage of the full match. Regardless of the amount of employer match, it’s a benefit that can add up over time and could help strengthen employees’ financial futures.

Increase contributions

In 2025, the annual limit on 401(k) or 403(b) plan contributions will increase $500 to $23,500. Encourage plan participants to bump up the amount they put into the plan each paycheck. Even a small increase can go a long way in helping to build a solid nest egg.

Get financial insight with Mutual of America’s resources

From videos and articles to essays and webinars, your employees have access to a wide array of content to help support their financial knowledge. You can also speak with your Mutual of America representative about financial education sessions relevant to your participants’ needs.

1EBRI Greenwald Research 2024 Workplace Wellness Survey, Page 23 (24 of PDF) https://www.ebri.org/docs/default-source/wbs/wws-2024/wws-2024_short-report.pdf

Better your tomorrow.

Contact your Mutual of America representative today.

Things

to know

1

Now you can request updates to participant service records online

As part of Mutual of America’s initiative to enhance plan administration self-service functionality, you now have the ability to request updates to participant service records in the plan sponsor portal. This enhanced functionality allows plan administrators to easily request changes to service record dates and add missing service records for employees.

2

Mutual of America feedback survey

Your satisfaction and feedback are incredibly valuable to us as we strive to continually improve our products and services. Each month, we randomly select plan sponsors to receive an email inviting them to share their feedback in a five-minute survey. We greatly value your business and appreciate your time responding to our surveys to help us serve you better.

3

New participant education videos

Our latest video series, “Preparing for Tomorrow,” consisting of four videos, is now available as part of the Retirement Reinvented program. The videos aim to teach participants foundational financial concepts by using cooking metaphors.